Takeaway From Japan’s 20-Year Malaise: The Danger of Delusional Thinking

September 13, 2010

The first was Yasushi Mieno, former Bank of Japan governor between December 1989 and 1994, who was credited with pricking Japan’s excess credit bubble and continued to have a strong influence on the Bank of Japan for many years afterward. The second was Kaoru Yosano, an ex-LDP veteran who is now the co-head of the LDP spin-off party “Tachi Agare Nippon,” a party sometimes described as party of “grumpy old men.” Mr. Osano was involved in the liquidation of the Senjyu, the specialist housing loan companies that were the first shot across the bow in Japan’s financial crisis. He also was an original member of the Structural Financial Reform Committee. He has also served as the chairman of the LDP’s policy research council, the tax research council, the economic and fiscal advisory committee, LDP chief cabinet secretary and as and economic and financial minister as well as treasury minister. The third is Heizo Takenaka, the ex-private sector economist who became the Junichiro Koizumi Cabinet’s financial minister and financial reform point man between 2002 and 2006.

Yasushi Mieno’s Version

As the man who pricked Japan's excess credit bubble that unleashed a crash in the stock and property markets and set Japan on course for a 20-year malaise, Mr. Mieno’s only regret is that he did not move sooner to deflate Japan's bubble. His excuse was that government was still trying to alleviate the negative impact of a strong yen and global equity markets were roiled by “Black Monday” in 1987. Thereafter, the MOF only agreed to rate hikes sufficient to keep a lid on inflation, not to address out-of-control asset prices.

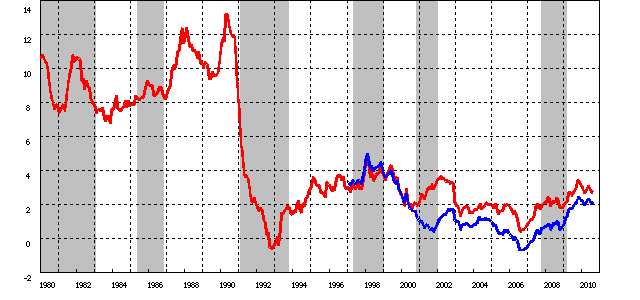

When he did move, Mr. Mieno and the Bank of Japan slammed on the monetary brakes hard, and kept their foot on the brakes too long. To deflate the bubble, Mr. Mieno and the BOJ raised Japan’s discount rate five times, to 6% in 1990. M2 money accelerated from 7% to 13% during the bubble between 1983 to 1990, but plunged precipitously to minus growth by 1992. In 1992, Japanese politicians and bureaucrats were divisively squabbling over how to pull the economy out of recession, with much of the criticism directed at the BOJ and Mr. Mieno, who rejected the idea that interest rates were strangling the economy, insisting there was no sharp economic downturn in sight and no need to stimulate the economy.

He admits that Japan’s response to the problem of excess non-performing debt in Japan’s financial sector was seriously impeded by delusional thinking, including,

a) What was termed the “convoy system” where the weaker companies in the banking system as well as other corporates were sheltered and supported by the healthier companies as well as the government, resulting in “zombie” companies that were neither alive nor dead.

b) No effective corporate governance of weaker banks, and

c) The myth that property prices, which were the primary collateral for a substantial amount of non-performing loans, always rose.

When the solvency issue first arose in the Senjyu and in certain credit unions around the summer of 1992, there was initially very strong political resistance to the use of public funds to address the problem. The Bank of Japan developed a countermeasure proposal and took it to the Ministry of Finance, but the MOF and the government in seeing the true scope of the latent losses among financial institutions, rejected the proposal because the potential losses were so large that using public funds did not seem viable.

While foreign economists generally believe that the BOJ’s failure to immediately and resolutely ease credit was one reason contributing to Japan’s structural deflation and long-term malaise, Mr. Mieno still doesn’t agree, pointing to the fact that Japan’s GDP growth accelerated from 1.5% to 2.3% in 1995, and reached 2.9% in 1996. In effect, however, a recalcitrant BOJ basically shot the government's all-out fiscal stimulus efforts in the foot, as teh government introduced six stimulus programs between 1992 and 1995 worth 65.5 trillion and cut income tax rates in 1994. Mr. Mieno claims the slowdown came despite such stimulus because of lack of response to major shift in Japan’s economy toward slower growth (restructuring), globalization and disruptive IT technology that exacerbated the negative after-effects of a burst bubble.

(Click to enlarge)

Kaoru Yosano Version

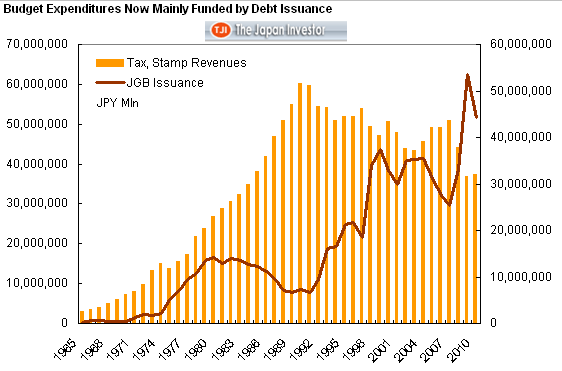

Kaoru Yosano believes that Japan has only about three years before a fiscal crisis, and that Japan must immediately to head off this crisis. Overall during the 1990s, Japan tried 10 fiscal stimulus packages totaling more than JPY100 trillion, with each failing to cure the recession. This "on-budget" government spending has caused public debt to exceed 100 percent of GDP (highest in the G7), and even more debt is apparent when the "off-budget" sector is included.

He sees the LDP’s inability to raise the consumption tax again as political weakness, and now nearly politically impossible. In October 2008, the Taro Aso Administration called for a consumption tax hike and lost, the DPJ’s Kan also renewed the public debate about the consumption tax, and his party also lost a significant number of seats. He blames the lack of political will to address Japan’s debt on the introduction of single seat electoral districts, which has resulted in all political parties simply seeking popularity, not doing what needs to get done.

But Mr.Yosano is not a casual observer. He was deputy chief cabinet secretary under the Hashimoto Administration. Ryutaro Hashimoto and his cabinet, mistakenly believed that Japan’s bad debt/balance sheet crisis was over by 1996 and moved toward fiscal consolidation, raising the consumption tax from 3% to 5% in April 1997, abolishing a JPY2 trillion tax break and basically increasing the burden on consumers by some JPY9 trillion. Mr. Yosano denies that these actions pushed Japan’s economy into a double-dip recession, instead pointing to the failures of Yamaichi Securities, Hokkaido Takushoku Bank and Sanyo Securities in the fall of the year. In particularl, the failure of Sanyo Securities in the call money market in Q3 nearly precipitated a melt-down in Japan’s banking system.

Further, he makes no mention of efforts at structural reform by the Hashimoto or other administrations he has been in (including the Abe and Aso administrations) because every attempt was thwarted by politicians in his own party that belonged to various special interest groups blocking such initiatives. In other words, while he has a sense of urgency about Japan's debt problem, he is very fuzzy about methods to do this other than raising the consumption tax about how Japan gets out of this mess.

Heizo Takenaka’s Version

For all the fuzzy logic we have had to suffer through from BOJ governors from Mr. Mieno onward to the current governor Masaaki Shirakawa, and an endless musical chairs of finance ministers and prime ministers, the ex-finance minister that makes the most sense is Heizo Takenaka, the point man for the Junichiro Koizumi Administration’s efforts to clean up the banking sector and restructure Japan’s economy.

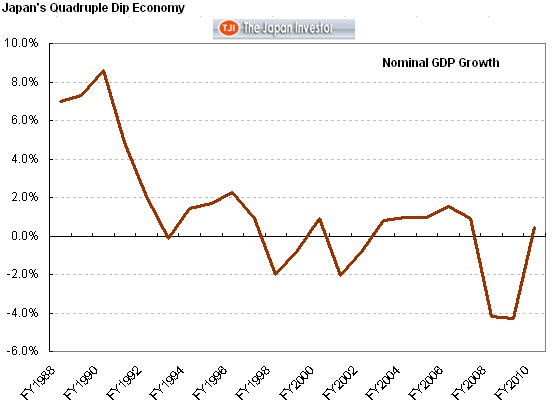

Mr. Takenaka describes Japan’s lost two decades as actually being three distinct periods. The first was “12 lost years” as Japan struggled to clean up the balance sheet mess from the bursting of the excess credit bubble, the second is “5 years of stability” under the Koizumi Administration, and the third is “the three worst lost years,” where there has been a systematic reversing of all the restructuring/reform initiatives under the Koizumi Administration. The first priority under the Koizumi Administration was a drastic clean-up of non-performing loans on the banks’ balance sheets. The banks and their political supporters were dragged kicking and screaming into cleaning up their balance sheets. While the Koizumi administration also pursued liberalization and institutional reforms such as the privatization of the post office, their efforts were vehemently resisted on every front, and not much real progress was made other than cleaning up the banks. As the banking crisis passed, Japan’s economy grew at an average of 2% per annum between 2003 and 2007, 70% of which was driven by domestic demand. The basic government fiscal balance improved from a deficit of JPY22 trillion to JPY6 trillion, or an amount equal to a consumption tax hike to 9%, and it looked like Japan was finally emerging from deflation.

Now, however, nominal GDP growth has dramatically declined, Japan has slipped back into deflation, Japan’s net debt has soared above 100% and government borrowings to fund the budget are now more than tax revenues.

Japan’s 20-Year Malaise: A Comedy of Policy Errors

The only encouraging progess was made between 2003 and 2007, when the Koizumi Administration cleaned up the banking sector NPLs and attempted to restructure Japan’s economy. Japan’s stock market bottomed in April 2003 at 7,600 and rallied to over 18,000 (137%). Since then, Japan has slipped back into malaise, deflation has returned and trend growth in government debt is accelerating, while stock prices have plummeted 58%.

To get Japan out of its current funk, Mr. Takenaka believes that a one-time massive infusion of fiscal stimulus is needed to eradicate a demand-supply gap still in the tens of trillions of yen range, spending the money on Haneda Airport and other clearly beneficial infrastructure projects, while pushing up growth in Japan’s M2 +CD money supply to 5%~6%--with the DPJ abandoning clearly unattainable election promises for something that actually works.

His suggestion of a big one-short stimulus package is reminiscent of what finance minister Korekiyo Takahashi did in 1931 in implementing a) massive one-time fiscal stimulus to eradicate a demand-supply gap, b) large issuance of JGBs to fund this and c) having the debt monetized by the BOJ. Mr. Takahashi’s actions were credited with ending the Showa Depression.

The Definition of Insanity: Doing the Same Thing Over and Over Again and Expecting a Different Result

Throughout the Heisei Malaise, Japan repeated the same policy formulas, i.e., wasteful public works expenditures and repeated interest rate cuts, while expecting different results. This is what Albert Einstein has said is the definition of insanity. While it was against their better judgement, the Bank of Japan tried quantitative easing without much success between March 2001 and March 2006. The MOF/BOJ also tried massive interventions of JPY20.5 trillion and JPY14.8 trillion in Q4 2003 and Q1 2004 respectively to stop JPY appreciation, yet here we are again at 15-year highs.

As an American myself, I do not believe it is in the nature of Americans to simply do the same thing over and over and expect a different result. Historically, we have kept hacking away at the problem until we get it right, but if Mr. Bernanke believes that more QE without solving the balance sheet issues at Fannie and Freddie and the housing bust, he too is delusional. President Obama is also delusional if he thinks that long-term investments to rebuild America's crumbling infrastructure and offering more money for small businesses will produce enough jobs to keep the Democrats from losing seats in the House of Representatives and the Senate given the extent and dept of the recession, as the additional stimulus needed given the US demand-supply gap is probably far larger, while the political will for additional large stimulus is just not there.

Basically, until the US solves its output gap problem, unemployment will remain uncomfortably high and the US economy will continue to act like Japan's near-comatose economy. Either the current administration and the Fed will keep tinkering with the problem until they get it right, or voters will vote out the Democrats and give the Republicans a shot at the problem. Let's hope someone gets the bright idea of combining comprehensive restructuring/balance sheet consolidation and eradication of zombie companies/institutions with accomodative monetary and fiscal policy--not just one of the above, but all of the above.

Source: Cullen Roche, Pragmatic Capitalism

The only encouraging progess was made between 2003 and 2007, when the Koizumi Administration cleaned up the banking sector NPLs and attempted to restructure Japan’s economy. Japan’s stock market bottomed in April 2003 at 7,600 and rallied to over 18,000 (137%). Since then, Japan has slipped back into malaise, deflation has returned and trend growth in government debt is accelerating, while stock prices have plummeted 58%.

To get Japan out of its current funk, Mr. Takenaka believes that a one-time massive infusion of fiscal stimulus is needed to eradicate a demand-supply gap still in the tens of trillions of yen range, spending the money on Haneda Airport and other clearly beneficial infrastructure projects, while pushing up growth in Japan’s M2 +CD money supply to 5%~6%--with the DPJ abandoning clearly unattainable election promises for something that actually works.

His suggestion of a big one-short stimulus package is reminiscent of what finance minister Korekiyo Takahashi did in 1931 in implementing a) massive one-time fiscal stimulus to eradicate a demand-supply gap, b) large issuance of JGBs to fund this and c) having the debt monetized by the BOJ. Mr. Takahashi’s actions were credited with ending the Showa Depression.

The Definition of Insanity: Doing the Same Thing Over and Over Again and Expecting a Different Result

Throughout the Heisei Malaise, Japan repeated the same policy formulas, i.e., wasteful public works expenditures and repeated interest rate cuts, while expecting different results. This is what Albert Einstein has said is the definition of insanity. While it was against their better judgement, the Bank of Japan tried quantitative easing without much success between March 2001 and March 2006. The MOF/BOJ also tried massive interventions of JPY20.5 trillion and JPY14.8 trillion in Q4 2003 and Q1 2004 respectively to stop JPY appreciation, yet here we are again at 15-year highs.

As an American myself, I do not believe it is in the nature of Americans to simply do the same thing over and over and expect a different result. Historically, we have kept hacking away at the problem until we get it right, but if Mr. Bernanke believes that more QE without solving the balance sheet issues at Fannie and Freddie and the housing bust, he too is delusional. President Obama is also delusional if he thinks that long-term investments to rebuild America's crumbling infrastructure and offering more money for small businesses will produce enough jobs to keep the Democrats from losing seats in the House of Representatives and the Senate given the extent and dept of the recession, as the additional stimulus needed given the US demand-supply gap is probably far larger, while the political will for additional large stimulus is just not there.

Basically, until the US solves its output gap problem, unemployment will remain uncomfortably high and the US economy will continue to act like Japan's near-comatose economy. Either the current administration and the Fed will keep tinkering with the problem until they get it right, or voters will vote out the Democrats and give the Republicans a shot at the problem. Let's hope someone gets the bright idea of combining comprehensive restructuring/balance sheet consolidation and eradication of zombie companies/institutions with accomodative monetary and fiscal policy--not just one of the above, but all of the above.

Source: Cullen Roche, Pragmatic Capitalism

No comments:

Post a Comment